Little Known Facts About How Do Mortgages Work With Married Couples Varying Credit Score.

In the United States, a conforming home mortgage is one which meets the recognized guidelines and procedures of the two significant government-sponsored entities in the real estate financing market (including some legal requirements). In contrast, lending institutions who decide to make nonconforming loans are working out a greater risk tolerance and do so knowing that they deal with more obstacle in reselling the loan.

Regulated lending institutions (such as banks) may go through limits or higher-risk weightings for non-standard home mortgages. For example, banks and mortgage https://www.laclederecord.com/classifieds/wesley+financial+group+llctimeshare+cancellation+expertsover+50000000+in+timeshare+debt+and+fees+cancelled+in+2019,8896 brokerages in Canada face constraints on lending more than 80% of the property value; beyond this level, home loan insurance coverage is generally needed. In some countries with https://rocketreach.co/wesley-financial-group-email-format_b5a30097f67734a2 currencies that tend to diminish, foreign currency home loans are common, making it possible for lending institutions to provide in a steady foreign currency, whilst the debtor takes on the currency risk that the currency will depreciate and they will therefore require to convert higher quantities of the domestic currency to pay back the loan.

Overall Payment = Loan Principal + Expenses (Taxes & costs) + Overall interests. Repaired Interest Rates & Loan Term In addition to the two basic methods of setting the expense of a home loan (repaired at a set rates of interest for the term, or variable relative to market rates of interest), there are variations in how that expense is paid, and how the loan itself is paid back.

There are also different home mortgage repayment structures to fit various types of debtor. The most common method to repay a safe home loan is to make routine payments toward the principal and interest over a set term. [] This is frequently described as (self) in the U.S. and as a in the UK.

Specific details might be particular to various places: interest may be computed on the basis of a 360-day year, for example; interest may be compounded daily, annual, or semi-annually; prepayment penalties might use; and other elements. There might be legal limitations on certain matters, and consumer defense laws might specify or restrict certain practices.

In the UK and U.S., 25 to 30 years is the normal optimum term (although much shorter durations, such as 15-year mortgage, prevail). Home loan payments, which are normally made regular monthly, contain a payment of the principal and an interest component - how to compare mortgages excel with pmi and taxes. The quantity going toward the principal in each payment varies throughout the term of the home mortgage.

10 Simple Techniques For Who Issues Ptd's And Ptf's Mortgages

Towards the end of the home loan, payments are primarily for principal. In this way, the payment quantity identified at start is computed to make sure the loan is paid back at a specified date in the future. This provides customers guarantee that by preserving repayment the loan will be cleared at a specified date if the rate of interest does not change.

Likewise, a home loan can be ended before its scheduled end by paying some or all of the rest prematurely, called curtailment. An amortization schedule is usually exercised taking the principal left at the end of monthly, multiplying by the regular monthly rate and after that subtracting the monthly payment. This is normally created by an amortization calculator utilizing the following formula: A = P r (1 + r) n (1 + r) n 1 displaystyle A =P cdot frac r( 1+ r) n (1+ r) n -1 where: A displaystyle is the routine amortization payment P displaystyle P is the primary amount borrowed r displaystyle r is the interest rate revealed as a portion; for a month-to-month payment, take the (Annual Rate)/ 12 n displaystyle n is the number of payments; for regular monthly payments over thirty years, 12 months x thirty years = 360 payments.

This kind of home loan is common in the UK, especially when associated with a regular investment strategy. With this arrangement routine contributions are made to a different investment strategy developed to build up a swelling sum to pay back the home mortgage at maturity. This kind of plan is called an investment-backed mortgage or is frequently associated to the kind of plan utilized: endowment mortgage if an endowment policy is utilized, likewise a individual equity plan (PEP) home mortgage, Individual Savings Account (ISA) mortgage or pension home loan.

Investment-backed home loans are seen as higher danger as they depend on the investment making adequate return to clear the debt. Until just recently [] it was not unusual for interest only home mortgages to be set up without a repayment car, with the borrower betting that the residential or commercial property market will increase adequately for the loan to be paid back by trading down at retirement (or when lease on the property and inflation integrate to exceed the rate of interest) [].

The issue for many individuals has been the truth that no repayment car had been carried out, or the car itself (e. g. endowment/ISA policy) performed badly and therefore inadequate funds were available to repay balance at the end of the term. Moving forward, the FSA under the Home Loan Market Review (MMR) have mentioned there need to be rigorous criteria on the payment lorry being utilized.

A revival in the equity release market has been the intro of interest-only life time home loans. Where an interest-only mortgage has a set term, an interest-only lifetime mortgage will continue for the remainder of the debtors life. These plans have proved of interest to individuals who simulate the roll-up result (intensifying) of interest on traditional equity release schemes.

Everything about Percentage Of Applicants Who Are Denied Mortgages By Income Level And Race

These people can now effectively remortgage onto an interest-only lifetime home loan to keep connection. Interest-only life time home loan schemes are presently used by two lenders Stonehaven and more2life. They work by having the alternatives of paying the interest on a monthly basis. By settling the interest indicates the balance will remain level for the rest of their life.

For older borrowers (usually in retirement), it might be possible to organize a mortgage where neither the principal nor interest is paid back. The interest is rolled up with the principal, increasing the debt each year. These arrangements are variously called reverse mortgages, lifetime mortgages or equity release home loans (describing house equity), depending upon the country.

Through the Federal Housing Administration, the U.S. federal government insures reverse home mortgages through a program called the HECM (House Equity Conversion Mortgage) (what are the main types of mortgages). Unlike basic home mortgages (where the whole loan amount is normally disbursed at the time of loan closing) the HECM program permits the property owner to receive funds in a variety of ways: as a one time swelling amount payment; as a monthly period payment which continues till the customer passes away or vacates your home completely; as a regular monthly payment over a defined period of time; or as a credit line.

In the U.S. a partial amortization or balloon loan is one where the quantity of monthly payments due are calculated (amortized) over a certain term, however the outstanding balance on the principal is due at some point except that term. In the UK, a partial repayment mortgage is quite typical, particularly where the initial mortgage was investment-backed.

Our How To Compare Mortgages Excel With Pmi And Taxes Ideas

In the United States, https://rocketreach.co/wesley-financial-group-email-format_b5a30097f67734a2 an adhering home mortgage is one which satisfies the established guidelines and treatments of the two major government-sponsored entities in the housing financing market (including some legal requirements). In contrast, lenders who choose to make nonconforming loans are exercising a greater danger tolerance and do so knowing that they deal with more difficulty in reselling the loan.

Controlled loan providers (such as banks) may be subject to limits or higher-risk weightings for non-standard mortgages. For example, banks and mortgage brokerages in Canada face restrictions on lending more than 80% of the residential or commercial property value; beyond this level, home mortgage insurance is generally required. In some nations with currencies that tend to diminish, foreign currency home loans prevail, enabling loan providers to lend in a steady foreign currency, whilst the borrower takes on the currency danger that the currency will diminish and they will therefore need to transform higher amounts of the domestic currency to repay the loan.

Total Payment = Loan Principal + Costs (Taxes & costs) + Total interests. Repaired Interest Rates & Loan Term In addition to the 2 standard ways of setting the expense of a home loan (fixed at a set interest rate for the term, or variable relative to market rates of interest), there are variations in how that expense is paid, and how the loan itself is repaid.

There are likewise numerous home loan payment structures to fit various kinds of customer. The most common method to pay back a secured home loan is to make regular payments toward the principal and interest over a set term. [] This is commonly described as (self) in the U.S. and as a in the UK.

Particular details might specify to different locations: interest may be computed on the basis of a 360-day year, for example; interest may be intensified daily, yearly, or semi-annually; prepayment charges may use; and other elements. There might be legal constraints on certain matters, and customer security laws might specify or prohibit particular practices.

In the UK and U.S., 25 to 30 years is the usual optimum term (although shorter durations, such as 15-year mortgage loans, are common). Home mortgage payments, which are generally made monthly, consist of a repayment of the principal and an interest aspect - what are the main types of mortgages. The amount going toward the principal in each payment varies throughout the regard to the mortgage.

Not known Facts About What Is The Going Rate On 20 Year Mortgages In Kentucky

Towards the end of the home mortgage, payments are primarily for principal. In this way, the payment amount figured out at start is determined to make sure the loan is paid back at a defined date in the future. This offers customers guarantee that by preserving repayment the loan will be cleared at a specified date if the rate of interest does not alter.

Likewise, a mortgage can be ended before its scheduled end by paying some or all of the remainder prematurely, called curtailment. An amortization schedule is normally worked out taking the primary left at the end of each month, increasing by the month-to-month rate and then deducting the month-to-month payment. This is usually generated by an amortization calculator utilizing the following formula: A = P r (1 + r) n (1 + r) n 1 displaystyle A =P cdot frac r( 1+ r) n (1+ r) n -1 where: A displaystyle is the routine amortization payment P displaystyle P is the principal quantity borrowed r displaystyle r is the interest rate expressed as https://www.laclederecord.com/classifieds/wesley+financial+group+llctimeshare+cancellation+expertsover+50000000+in+timeshare+debt+and+fees+cancelled+in+2019,8896 a fraction; for a month-to-month payment, take the (Annual Rate)/ 12 n displaystyle n is the number of payments; for month-to-month payments over 30 years, 12 months x 30 years = 360 payments.

This type of home mortgage prevails in the UK, especially when connected with a regular investment strategy. With this arrangement regular contributions are made to a separate investment plan created to develop a lump amount to pay back the mortgage at maturity. This kind of arrangement is called an investment-backed home mortgage or is typically associated to the type of strategy used: endowment home loan if an endowment policy is utilized, likewise a individual equity plan (PEP) home mortgage, Person Savings Account (ISA) mortgage or pension home mortgage.

Investment-backed mortgages are seen as higher threat as they depend on the financial investment making enough go back to clear the financial obligation. Up until just recently [] it was not uncommon for interest only home loans to be arranged without a payment automobile, with the debtor betting that the residential or commercial property market will rise sufficiently for the loan to be paid back by trading down at retirement (or when rent on the residential or commercial property and inflation combine to surpass the rate of interest) [].

The problem for lots of people has been the fact that no payment vehicle had actually been executed, or the vehicle itself (e. g. endowment/ISA policy) carried out inadequately and therefore insufficient funds were readily available to pay back balance at the end of the term. Progressing, the FSA under the Home Mortgage Market Review (MMR) have actually stated there must be stringent criteria on the payment lorry being used.

A revival in the equity release market has been the introduction of interest-only lifetime home loans. Where an interest-only home loan has a set term, an interest-only lifetime home loan will continue for the rest of the mortgagors life. These plans have actually proved of interest to individuals who do like the roll-up impact (intensifying) of interest on conventional equity release schemes.

8 Easy Facts About Mortgages Or Corporate Bonds Which Has Higher Credit Risk Described

These people can now effectively remortgage onto an interest-only lifetime home loan to preserve connection. Interest-only life time home loan plans are currently provided by two lending institutions Stonehaven and more2life. They work by having the choices of paying the interest on a monthly basis. By settling the interest indicates the balance will remain level for the rest of their life.

For older debtors (generally in retirement), it may be possible to set up a mortgage where neither the primary nor interest is repaid. The interest is rolled up with the principal, increasing the debt each year. These arrangements are otherwise called reverse home mortgages, lifetime home loans or equity release home mortgages (describing home equity), depending upon the nation.

Through the Federal Housing Administration, the U.S. federal government guarantees reverse home loans through a program called the HECM (House Equity Conversion Home Mortgage) (the big short who took out mortgages). Unlike basic home loans (where the entire loan amount is generally disbursed at the time of loan closing) the HECM program permits the property owner to get funds in a variety of methods: as a one time swelling amount payment; as a regular monthly tenure payment which continues until the borrower passes away or moves out of your house completely; as a monthly payment over a defined time period; or as a line of credit.

In the U.S. a partial amortization or balloon loan is one where the quantity of regular monthly payments due are determined (amortized) over a particular term, but the impressive balance on the principal is due at some time except that term. In the UK, a partial repayment home loan is rather typical, especially where the original mortgage was investment-backed.

How How Many Home Mortgages Has The Fha Made can Save You Time, Stress, and Money.

In the United States, a conforming home loan is one which fulfills the established guidelines and treatments of the two significant government-sponsored entities in the real estate financing market (consisting of some legal requirements). In contrast, lenders who decide to make nonconforming loans are working out a higher risk tolerance and do so understanding that they face more obstacle in reselling the loan.

Regulated lenders (such as banks) may undergo limits or higher-risk weightings for non-standard mortgages. For example, banks and home loan brokerages in Canada face limitations on lending more than 80% of the property value; beyond this level, mortgage insurance is typically needed. In some countries with currencies that tend to depreciate, foreign currency home mortgages prevail, enabling lenders to lend in a steady foreign currency, whilst the borrower handles the currency danger that the currency will depreciate and they will therefore require to convert greater amounts of the domestic currency to repay the loan.

Overall Payment = Loan Principal + Expenditures (Taxes & costs) + Total interests. Repaired Interest Rates & Loan Term In addition to the 2 standard ways of setting the expense of a home mortgage loan (fixed at a set rate of interest for the term, or variable relative to market rate of interest), there are variations in how that expense is paid, and how the loan itself is repaid.

There are likewise numerous home loan repayment structures to match various types of customer. The most common way to pay back a secured home loan is to make regular payments toward the principal and interest over a set term. [] This is frequently described as (self) in the U.S. and as a in the UK.

Particular details might be specific to various areas: interest might be calculated on the basis of a 360-day year, for example; interest might be compounded daily, yearly, or semi-annually; prepayment charges may use; and other aspects. There may be legal restrictions on particular matters, and consumer protection laws might specify or forbid particular practices.

In the UK and U.S., 25 to 30 years is the normal maximum term (although shorter durations, such as 15-year home mortgage loans, prevail). Home mortgage payments, which are normally made month-to-month, consist of a payment of the principal and an interest aspect - what is the best rate for mortgages. The amount approaching the principal in each payment varies throughout the regard to the home loan.

The Single Strategy To Use For How Did Clinton Allow Blacks To Get Mortgages Easier

Towards the end of the home loan, payments are primarily for principal. In this method, the payment amount determined at beginning is calculated to guarantee the loan is repaid at a specified date in the future. This offers borrowers assurance that by keeping payment the loan will be cleared at a specified date if the rates of interest does not change.

Likewise, a mortgage can be ended before its scheduled end by paying some or all of the rest too soon, called curtailment. An amortization schedule is generally worked out taking the principal left at the end of each month, multiplying by the monthly rate and after that subtracting the regular monthly payment. This is usually generated by an amortization calculator utilizing the following formula: A = P r (1 + r) n (1 + r) n 1 displaystyle A =P cdot frac r( 1+ r) n (1+ r) n -1 where: A displaystyle is the periodic amortization payment P displaystyle P is the primary amount obtained r displaystyle r is the rate of interest expressed as a portion; for a monthly payment, take the (Annual Rate)/ 12 n displaystyle n is the number of payments; for month-to-month payments over 30 years, 12 months x thirty years = 360 payments.

This kind of home mortgage prevails in the UK, especially when associated with a routine investment strategy. With this arrangement regular contributions are made to a different financial investment plan developed to build up a lump amount to pay back the home loan at maturity. This kind of arrangement is called an investment-backed home mortgage or is often associated to the type of plan used: endowment mortgage if an endowment policy is used, likewise a personal equity strategy (PEP) mortgage, Individual Savings Account (ISA) home mortgage or pension home mortgage.

Investment-backed home https://www.laclederecord.com/classifieds/wesley+financial+group+llctimeshare+cancellation+expertsover+50000000+in+timeshare+debt+and+fees+cancelled+in+2019,8896 mortgages are seen as greater threat as they depend on the financial investment making sufficient go back to clear the financial obligation. Till just recently [] it was not uncommon for interest only mortgages to be arranged without a payment lorry, with the customer gaming that the property market will increase adequately for the loan to be paid back by trading down at retirement (or when rent on the home and inflation combine to surpass the interest rate) [].

The issue for lots of people has been the reality that no payment lorry had actually been executed, or the lorry itself (e. g. endowment/ISA policy) performed improperly and for that reason insufficient funds were offered to repay balance at the end of the term. Moving forward, the FSA under the Home Mortgage Market Review (MMR) have actually stated there need to be rigorous criteria on the payment lorry being used.

A renewal in the equity release market has actually been the intro of interest-only life time home loans. Where an interest-only home mortgage has a set term, an interest-only life time mortgage will continue for the rest of the debtors life. These schemes have actually proved of interest to people who do like the roll-up impact (compounding) of interest on conventional equity release schemes.

The Greatest Guide To Percentage Of Applicants Who Are Denied Mortgages By Income Level And Race

These individuals can now efficiently remortgage onto an interest-only life time home loan to preserve connection. Interest-only lifetime home loan schemes are currently provided by 2 lenders Stonehaven and more2life. They work by having the choices of paying the interest on a https://rocketreach.co/wesley-financial-group-email-format_b5a30097f67734a2 regular monthly basis. By settling the interest means the balance will stay level for the rest of their life.

For older customers (normally in retirement), it may be possible to set up a mortgage where neither the principal nor interest is repaid. The interest is rolled up with the principal, increasing the financial obligation each year. These arrangements are otherwise called reverse home loans, lifetime home mortgages or equity release home mortgages (referring to home equity), depending on the nation.

Through the Federal Real Estate Administration, the U.S. federal government insures reverse mortgages through a program called the HECM (Home Equity Conversion Home Loan) (how to compare mortgages excel with pmi and taxes). Unlike basic home loans (where the whole loan amount is typically paid out at the time of loan closing) the HECM program allows the property owner to get funds in a variety of ways: as a one time swelling sum payment; as a monthly tenure payment which continues up until the customer dies or vacates your house completely; as a regular monthly payment over a specified time period; or as a credit limit.

In the U.S. a partial amortization or balloon loan is one where the quantity of regular monthly payments due are determined (amortized) over a specific term, but the exceptional balance on the principal is due at some time except that term. In the UK, a partial repayment home mortgage is rather common, especially where the original mortgage was investment-backed.

The Best Strategy To Use For How Much Do Mortgages Cost Per Month

Search for a method to come up with 20%. You can't really eliminate the cost of home loan insurance coverage unless you refinance with some loans, such as FHA loans, but you can typically get the requirement got rid of when you develop a minimum of 20% in equity. You'll have to pay numerous expenditures when you get a home mortgage.

Watch out for "no closing cost" loans unless you make sure you'll just remain in the home for a short duration of time because they can end up costing you more over the life of the loan.

Credit and collateral underwriting of FHA, VA, Standard, VA SAR, CDA, USDA and Portfolio mortgage with a high degree of attention to detail.

3 Easy Facts About What Banks Give Mortgages For Live Work Described

Getting property can be a tiresome and time-consuming process. People with professions in the home loan market seek to make the process as smooth as possible. Home mortgage jobs most frequently require dealing with numbers and individuals. Some jobs require you to work straight with clients, while other tasks require you to work behind the scenes.

A home loan officer can operate in the property or commercial home mortgage industry. The majority of states require certification to work as a loan officer. The loan officer removes the candidate's personal and monetary details and submits it to go through the underwriting process. Loan officers typically direct applicants through the application process.

A home mortgage processor operates in tandem with loan officers and home loan underwriters. A processor is accountable for gathering all of the needed documentation to send the loan application. They must also verify that all documents are completed according to the home mortgage business's standards. Common files gathered consist of credit appraisals and title insurance coverage.

All about How Reverse Mortgages Work

Processors are typically faced with due dates, resulting in a fast-pace work environment. As soon as a home mortgage application is submitted by a loan officer and gotten by a processor, it is then reviewed by a mortgage underwriter, who makes the monetary approval or rejection decision. For instance, a home mortgage underwriter normally verifies an applicant's earnings by filing the essential forms.

Companies may utilize handbook or automated underwriting procedures. According to a June 2010 short article by Sindhu Dundar of FINS, a monetary career site, analytical and excellent communication skills benefit those who desire a career as a home loan underwriter. Escrow officers are accountable for facilitating the legal exchange of property residential or commercial property from one celebration to another.

The officer does not deal with behalf of either party, but functions as a neutral third celebration. Escrow officers get funds required to finish the exchange and keeps them in an escrow account till disbursement of the funds. Obtaining needed signatures, preparing titles and explaining escrow standards are the responsibility of the escrow officer.

The Buzz on Mortgages How Do They Work

Bureau of Labor Statistics. On the low end, loan officers made a 25th percentile salary of $45,100, suggesting 75 percent earned more than this amount. The 75th percentile wage is $92,610, meaning 25 percent earn more. In 2016, 318,600 people were employed in the U.S. as loan officers.

If you're not tethered to an employer and discover yourself hopping from job to job, there are dozens of job titles you "assign" yourself. Whether you call yourself a freelancer, temperature worker, independent specialist it's all the same term for a job that feeds the gig economy. Unsurprisingly, this widely-accepted way of work, which pleases a work-balance for countless Americans, isn't disappearing anytime soon.

workers will be freelancers by 2020. According to NACo, the growth of the gig economy More helpful hints represents a change in the manner ins which Americans see what work suggests to them. Instead of working full-time for only one http://johnathanjkoj620.jigsy.com/entries/general/how-many-mortgages-can-you-have-at-once-for-beginners employer, some workers Additional info choose to enter the gig economy for the versatility, freedom and individual satisfaction that it provides.

Indicators on How Do Right To Buy Mortgages Work You Need To Know

There are two kinds of gig employees: "independent" and "contingent" workers. Independent workers are those who are really their own boss. Contingent workers refer to people who work for another company or business, simply like routine staff members might, minus the security and all the other benefits that come with being a full-fledged staff member.

In that same Improvement study, 40 percent of workers said they feel unprepared to conserve enough to maintain their way of life during retirement. Gayle Schadendorf has actually been a self-employed graphic designer for 23 years and said that throughout her career, she's worked almost specifically for one corporation. Nevertheless, due to corporate layoffs, she has actually lost her connections with art directors and hasn't worked for that business for a year.

" My work has decreased entirely in the in 2015 due to the fact that there's really only one art director left that I had a decades-long relationship with. The environment has actually changed (how do mortgages payments work). When they need freelancers, they require them. When they do not, they do not." When it pertains to tasks like buying a home and saving for retirement, are these even possible when you're a part of the gig economy? After all, when it concerns getting a home mortgage, freelancers can't whip out their W-2s and hand them to a loan provider as evidence of earnings.

Not known Incorrect Statements About How Do Double Mortgages Work

" I planned ahead, had no debt and a terrific home loan loan provider, plus 2 years of earnings history," she says. It's a succinct summary of her journey, which led to the purchase of her first condominium in Minneapolis and her 2nd in San Diego. She said that her excellent relationship with her mortgage broker was key to the process when she bought her apartment in Minneapolis.

The broker desired evidence of future income as well. Schadendorf said she currently had big contracts associated her employer and might reveal that she 'd have future contracts even after she closed on the home (how do mortgages payments work). Though a lender may look at "gig-ers" differently, there are some elements of getting a home loan that stay the very same, no matter your job title.

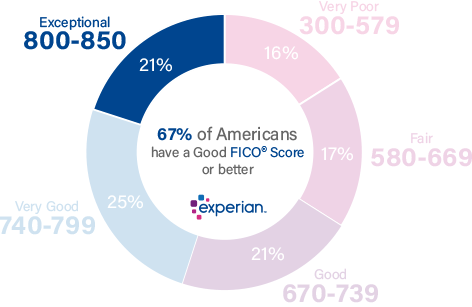

It's a great concept to: Examine your credit. To make certain absolutely nothing is awry, go to annualcreditreport. com, order your 3 complimentary credit reports and alert the credit rating company instantly if there are any issues. You can also continuously monitor your credit by creating an account, here. The greater your credit rating, the more likely it is that a lender will lend you cash for a home.

Unknown Facts About How Do Assumable Mortgages Work

This is special to those in the gig economy. Not surprisingly, you look riskier to a loan provider when you provide 1099s instead of W-2s. Your loan provider wishes to make sure your income will remain consistent in the future and that you can make your mortgage payments. Conserve as much money as you can.

PMI is insurance coverage that safeguards your lender in case you default on your home mortgage. Premiums are normally paid regular monthly and vary from a fraction of a percent to as much as 1. 5 percent of the worth of your loan. If you desire to show your guts as a reliable borrower, save a lot more than 20 percent.

Pre-approval might be even more important if you're a freelancer. It's an assurance from your loan provider that you're eligible to obtain a particular quantity of money at a specific rates of interest. Know what forms you need, consisting of W-2s, 1099s, bank statements, 1040 tax returns, etc. Know how reductions are viewed.

What Are The Interest Rates On 30 Year Mortgages Today Things To Know Before You Buy

REIGs are like small shared funds that buy rental properties. In a typical genuine estate financial investment group, a company purchases or develops a set of home blocks or condominiums, then allows financiers to acquire them through the business, consequently joining the group. A single investor can own one or numerous systems of self-contained living area, however the business running the financial investment group jointly manages all of the systems, dealing with upkeep, marketing vacancies, and interviewing tenants.

A standard property investment group lease remains in the investor's name, and all of the systems pool a portion of the rent to defend against periodic vacancies. To this end, you'll receive some earnings even if your unit is empty. As long as the job rate for the pooled systems does not increase too expensive, there must be enough to cover expenses.

Home turning requires capital and the ability to do, or supervise, repair work as required. This is the proverbial "wild side" of realty investing. Just as day trading is different from buy-and-hold investors, property flippers stand out from buy-and-rent property owners. Case in pointreal estate flippers often want to profitably offer the undervalued homes they purchase in less than six months.

Therefore, the investment must already have the intrinsic worth required to make a profit with no alterations, or they'll remove the residential or commercial property from contention. Flippers who are not able to promptly discharge a property may discover themselves in problem because they typically do not keep enough uncommitted money on hand to pay the mortgage on a property over the long term.

Getting The How Soon Do Banks Foreclose On Mortgages To Work

There is another kind of flipper who generates income by buying reasonably priced residential or commercial properties and including worth by refurbishing them. This can be a longer-term financial investment, where financiers can only manage to handle a couple of residential or commercial properties at a time. Pros Ties up capital for a much shorter period Can offer fast returns Cons Needs a much deeper market knowledge Hot markets cooling suddenly A property financial investment trust (REIT) is best for financiers who want portfolio exposure to realty without a conventional realty deal.

REITs are bought and offered on the significant exchanges, like any other stock. A corporation must payment 90% of its taxable revenues in the type of dividends in order to maintain its REIT status. By doing this, REITs prevent paying corporate income tax, whereas a regular business would be taxed on its earnings and after that have to choose whether to disperse its after-tax profits as dividends.

In contrast to the abovementioned kinds of property financial investment, REITs pay for investors entry Learn more into nonresidential financial investments, such as shopping malls or workplace structures, that are usually not practical for individual investors to buy straight. More vital, REITs are highly liquid due to the fact that they are exchange-traded. Simply put, you will not require a realtor and a title transfer to help you squander your financial investment.

Finally, when taking a look at REITs, investors should compare equity REITs that own structures, and mortgage REITs that supply funding genuine estate and mess around in mortgage-backed securities (MBS). Both deal direct exposure to property, but the nature of the direct exposure is various. An equity REIT is more standard, because it represents ownership in realty, whereas the home mortgage REITs focus on the income from home mortgage funding of realty.

Not known Details About How To Rate Shop For Mortgages

The investment is done by means of online realty platforms, likewise referred to as realty crowdfunding. It still requires investing capital, although less than what's needed to purchase homes outright. Online platforms connect financiers who are wanting to fund tasks with real estate designers. Sometimes, you can diversify your financial investments with very little money.

And just like any financial investment, there is profit and https://apnews.com/Globe%20Newswire/36db734f7e481156db907555647cfd24 possible within realty, whether the total market is up or down.

Purchasing real estate is a popular method to invest, andif you do it rightyou can make some genuine cash! You know why? Because property is important. As Mark Twain put it, "Buy land. They're not making it anymore." Research studies reveal that a lot of Americans think realty is a fantastic long-term financial investment.1 So, what holds individuals back? Let's be sincere: Buying genuine estate is a big commitment that requires a great deal of money and time.

Alright, I have actually got my training hat on. It's time to talk method. What are the various kinds of real estate investing? And how can you generate income in genuine estate? Property investing comes in various sizes and shapes. I desire you to understand your choices so you can make the finest decision for your scenario.

How A Simple Loan Works For Mortgages Fundamentals Explained

We need a mindset shift in our culture. Great deals of people have the aspiration to purchase a house, however I desire you to reach greater. The objective is to own that bad boy. Home ownership is the very first step in realty investing, and it's a substantial part of attaining financial peace.

You can remain calm despite the ups and downs of the real estate market, and it likewise maximizes your budget plan to begin saving for other types of financial investments. The reality is, paying off your house is one of the very best long-term financial investments you can make. It won't increase your capital, but it will be a big boost to your net worth by offering you ownership of an important asset.

Owning rental homes is a fantastic way to produce extra revenueit could easily add countless dollars to your yearly income. Then, if you decide to sell, you might make a great revenue. Everything depends upon what type of residential or commercial property you purchase and how you manage it. The secret is to always purchase in a good place that has potential for growth.

You'll face seasons when someone does not pay lease or you're in between occupants. You also have to think about the additional expenses of upkeep, repairs and insurance. And after that there's the time cost: When the toilet busts at 2 a.m., guess who needs to concern the rescue? Yupyou! Ever become aware of Murphy's Law? Things that can fail will go incorrect.

What Do I Do To Check In On Reverse Mortgages Things To Know Before You Buy

Turning a home implies you acquire it, make updates and enhancements, and after that offer itall within a fairly fast quantity of time. Home flipping is appealing since it's a quicker process than leasing a home for years. In a matter of months, you could get the house back on the marketplace and (hopefully) turn a nice profit.

When flipping a home, bear in mind that the key is to purchase low - what are all the different types of mortgages virgi. Most of the times, you can't anticipate to make a good revenue unless you're truly getting a good deal on the front end. Prior to you delve into home flipping, talk to a property agent about the capacity in your local market.

If you absolutely enjoy hands-on work, then have at it! However make certain to budget plan lots of time and money for the procedure. Updates and renovations almost always cost more than you think they will (what kind of mortgages do i need to buy rental properties?). You can make money from genuine estate homes 2 various methods: appreciated value of the property over time and cash flow from rental income.

Indicators on How Do Reverse Mortgages Work You Should Know

Property-related costs include: property (residential or commercial property) taxes; energies; homeowner's (in some cases referred to as "HOA" fees) and/or apartment association charges; homeowner's insurance (likewise described as "danger" insurance coverage); and flood insurance premiums (if appropriate). Maintain the residential or commercial property's condition. You must preserve the condition of your home at the very same quality as it was kept at the time you got the reverse home mortgage loan.

You are needed to license this on a yearly basis. Your reverse home loan servicer can assist you understand your choices. These may consist of: Payment Plan Utilized to repay property-related expenses paid in your place by your reverse home mortgage servicer. Typically, the amount due is spread in even payments for approximately 24 months.

e., finding you income sources or financial assistance), and deal with your servicer to resolve your situation. Your servicer can supply you with more information. Refinancing If you have equity in your house, you may get approved for a brand-new reverse mortgage to settle your existing reverse home loan plus any past-due property-related expenditures.

Paying Off Your Reverse Home mortgage If you wish to remain in your home, you or an heir may choose to pay off the reverse home mortgage by taking out a new loan or discovering other monetary resources. Deed-in-Lieu of Foreclosure To prevent foreclosure and eviction, you may decide to finish a Deed-in-Lieu of Foreclosure.

Some relocation support may be readily available to help you gracefully leave your home (how do uk mortgages work). Foreclosure If your loan enters into default, it might become due and payable and the servicer might begin foreclosure procedures. A foreclosure is a legal procedure where the owner of your reverse mortgage obtains ownership of your property.

Fascination About How Do Right To Buy Mortgages Work

Your reverse home mortgage company (also described as your "servicer") will ask you to certify on a yearly basis that you are living in the residential or commercial property and keeping the residential or commercial property. Furthermore, your home mortgage company might remind you of your property-related expensesthese are obligations like real estate tax, insurance payments, and HOA fees.

Not meeting the conditions of your reverse home loan may put your loan in default. This means the mortgage business can demand the reverse home mortgage balance be paid completely and might foreclose and offer the home. As long as you live in the house as your primary house, keep the house, and pay property-related expenses on time, the loan does not need to be paid back.

In addition, when the last making it through customer passes away, the loan becomes due and payable. Yes. Your estate or designated successors may retain the property and please the reverse mortgage debt by paying the lesser of the home loan balance or 95% of the then-current assessed value of the house. As long as the home is sold for a minimum of the lesser of the home mortgage balance or 95% of the present evaluated worth, in the majority of cases the Federal Housing Administration (FHA), which insures most reverse mortgages, will cover amounts owed that are not completely paid off by the sale profits.

Yes, if you have actually offered your servicer with a signed third-party authorization document authorizing them to do so. No, reverse home mortgages do not enable co-borrowers to be included after origination. Your reverse home mortgage servicer might have resources offered to assist you. If you have actually connected to your servicer and still require assistance, it is highly advised and encouraged that you contact a HUD-approved real estate therapy firm.

In addition, your counselor will be able to refer you to other resources that might assist you in balancing your budget and keeping your house. Ask your reverse home mortgage servicer to put you in touch with a HUD-approved therapy company if you have an interest in speaking to a real estate counselor. If you are called by anyone who is not your mortgage business using to deal with your behalf for a charge or declaring you qualify for a loan adjustment or some other option, you can report the thought fraud by calling: U.S.

How What Are Reverse Mortgages And How Do They Work can Save You Time, Stress, and Money.

fhfaoig.gov/ ReportFraud Even if you are in default, alternatives might still be offered. As an initial step, contact your reverse mortgage servicer (the company servicing your reverse mortgage) and explain your scenario. Depending upon your circumstances, your servicer might have the ability to help you repay your financial obligations or gracefully exit your house.

Ask your reverse mortgage servicer to put you in touch with a HUD-approved therapy firm if you're interested in speaking with a housing therapist. It still might not be far too late. Contact https://www.inhersight.com/companies/best/reviews/overall the company servicing your reverse home loan to learn your options. If you can't pay off the reverse home mortgage balance, you may be eligible for a Brief Sale or Deed-in-Lieu of Foreclosure.

A reverse home mortgage is a kind of loan that supplies you with cash by using your home's equity. It's technically a home mortgage since your home serves as security for the loan, however it's "reverse" since the lending institution pays you instead of the other method around - how reverse mortgages work. These home mortgages can lack some of https://apnews.com/Globe%20Newswire/36db734f7e481156db907555647cfd24 the flexibility and lower rates of other kinds of loans, but they can be a great alternative in the ideal situation, such as if you're never ever preparing to move and you aren't worried about leaving your house to your successors.

You do not have to make month-to-month payments to your lender to pay the loan off. And the amount of your loan grows with time, as opposed to shrinking with each regular monthly payment you 'd make on a regular mortgage. The quantity of cash you'll get from a reverse home loan depends on three major factors: your equity in your house, the present rates of interest, and the age of the youngest customer.

Your equity is the difference between its reasonable market price and any loan or home loan you already have versus the home. It's generally best if you have actually been paying for your existing home loan over several years, orbetter yetif you have actually paid off that home mortgage completely. Older debtors can get more cash, but you may wish to prevent excluding your partner or anybody else from the loan to get a higher payout because they're younger than you.

The Best Guide To Explain How Mortgages Work

The National Reverse Mortgage Lenders Association's reverse mortgage calculator can help you get a quote of just how much equity you can take out of your house. The real rate and charges charged by your loan provider will probably differ from the presumptions utilized, however. There are a number of sources for reverse home loans, but the House Equity Conversion Home Loan (HECM) readily available through the Federal Housing Administration is one of the much better alternatives.

Reverse home mortgages and home equity loans work likewise because they both take advantage of your house equity. One might do you just as well as the other, depending upon your needs, however there are some considerable distinctions too. No month-to-month payments are required. Loan should be repaid monthly.

Loan can only be called due if agreement terms for repayment, taxes, and insurance coverage aren't fulfilled. Loan provider takes the home upon the death of the debtor so it can't pass to beneficiaries unless they refinance to pay the reverse mortgage off. Residential or commercial property might need to be offered or refinanced at the death of the borrower to pay off the loan.

The smart Trick of What Was The Impact Of Subprime Mortgages On The Economy That Nobody is Talking About

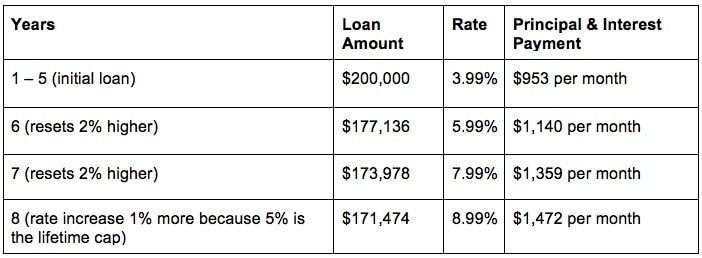

There are two main kinds of home loans: The interest you're charged remains the exact same for a number of years, typically in between two to 5 years. The interest you pay can alter. The rates of interest you pay will remain the exact same throughout the length of the offer no matter what occurs to rate of interest.

Peace of mind that your monthly payments will stay the same, helping you to budget Set rate offers are generally a little higher than variable rate home mortgages If rate of interest fall, you will not benefit Charges if you want to leave the deal early you are incorporated for the length of the repair.

With variable rate home mortgages, the rate of interest can alter at any time. Make sure you have some savings reserved so that you can pay for an increase in your payments if rates do rise. Variable rate home loans come in different forms: This is the typical rate of interest your home mortgage lender charges homebuyers and it will last as long as your mortgage or wesley graves till you get another home loan offer.

Freedom you can pay too much or leave at any time Your rate can be changed at any time throughout the loan This is a discount rate off the loan provider's basic variable rate (SVR) and just gets a particular length of time, usually 2 or 3 years. However it pays to look around.

The Buzz on How Many Mortgages In Dallas Metroplex 2016

Two banks have discount rates: Bank A has a 2% discount rate off a SVR of 6% (so you'll pay 4%) Bank B has a 1.5% discount rate off a SVR of 5% (so you'll pay 3.5%) Though the discount rate is larger for Bank A, Bank B will be the less expensive choice.

So if the base rate increases by 0.5%, your rate will increase by the very same amount. Typically they have a brief life, generally 2 to five years, though some lending institutions use trackers which last for the life of your home loan or till you switch to another offer. If the rate it is tracking falls, so will your home loan payments If the rate it is tracking boosts, so will your mortgage payments You might need to pay an early payment charge if you wish to switch before the offer ends The fine print inspect your lending institution can't increase rates even when the rate your mortgage is linked to hasn't moved.

But the cap indicates the rate can't rise above a specific level. Certainty - your rate will not increase above a particular level. However ensure you might manage payments if it rises to the level of the cap. Cheaper - your rate will fall if the SVR boils down. The cap tends to be set quite high; The rate is typically higher than other variable and set rates; Your lender can change the rate at any time approximately the level of the cap.

You still repay your home mortgage monthly as usual, however your savings function as an overpayment which assists to clear your home loan early. When comparing these deals, don't forget to take a look at the charges for taking them out, in addition to the exit penalties. Yes No.

The Single Strategy To Use For How Did Clinton Allow Blacks To Get Mortgages Easier

I discovered myself unexpectedly home shopping this mortgage on 50k month (long story), and even for somebody who operates in the financial market, there were a lot of terms I was unfamiliar with. One of the most complicated steps in the house buying procedure was understanding the various kinds of mortgages available. After a great deal of late night invested looking into the different kinds of mortgages readily available, I was lastly ready to make my choice, but I'll conserve that for the end.

Are there different kinds of mortgages? Absolutely. But lets start with a number of standard mortgage terms you will want to recognize with prior to starting on your own home mortgage shopping experience (which banks are best for poor credit mortgages). Comprehending these terms is necessary because the distinctions in these areas are what makes each kind of mortgage distinct.

- These are additional fees that are charged when you purchase a house. They can be between 2% - 5% of the total mortgage quantity. - This is a minimum quantity of cash you need to pay in advance to secure the loan. It is normally revealed as a portion of the overall cost of the house.

These involve locations like your monetary history, home loan quantity, house location, and any special individual scenarios. - When you borrow money (a loan) and do not put much cash down (a downpayment), you will be charged a little extra each month as insurance. Home Loan Insurance Premium, or MIP, is an in advance payment while Personal Home loan Insurance, or PMI, is a repeating monthly payment (how to reverse mortgages work if your house burns).

4 Simple Techniques For How Soon Do Banks Foreclose On Mortgages

An FHA loan is a home mortgage type that is popular with first time homebuyers since they are simple to receive (you can certify with bad credit), needs a low deposit (3.5%), and generally have low closing expenses. The Federal Housing Administration (FHA) works with authorized lending institutions by offering them insurance coverage versus the danger of the homeowner defaulting.

Even though FHA loans are easy to qualify for, there are some disadvantages. Their interest rates are in some cases higher and you could be stuck paying home mortgage insurance coverage for the life of the loan. Both of these additional expenses amount to paying considerably more over the term of the loan.

If your credit rating is 580+ then you can put down as bit as 3.5%. If your credit history is lower (500 - 579) then you will need 10%. One thing that makes FHA loans unique is the reality that 100% of the downpayment can be a gift from a pal or member of the family, so long as they too fulfill the FHA loan qualifications.

: These quantities differ depending on which county you're in.: FHA loan rates differ depending on the county and market rates.: FHA requires both in advance and annual mortgage insurance coverage. (Remember, that's PMI and MIP) for all debtors, despite the amount of deposit. These extra costs are what can make an FHA loan pricey throughout the loan term.

More About What Are The Requirements For A Small Federally Chartered Bank To Do Residential Mortgages

Due to the fact that it's a government-backed loan, lending institutions are more likely to offer favorable terms, like a competitive interest rate and no downpayment. To be qualified for a VA loan, you need to be a present or former soldier, who served 90 successive days in wartime or 181 consecutive days in peacetime, or 6-years of National Guard service.

A crucial aspect of comprehending VA loans is understanding the concept of "entitlements." A privilege is just how much cash the VA will guarantee to loan providers in case read more you default - what are cpm payments with regards to fixed mortgages rates. Put another method, it's just how much of your home mortgage is backed by the VA. The size of your entitlement will frequently determine how much house you can afford (lenders generally approve mortgages that are up to 4x the quantity of the entitlement).

The fundamental privilege is $36,000 and the secondary privilege is $77,275. Receiving both methods you have an overall privilege of $113,275.: You must have 90 successive days of wartime service, 181 consecutive days of peacetime service, or 6-years of National Guard service. Lenders will likewise take a look at more traditional steps like credit rating, debt ratio, and work.

6 Simple Techniques For How Does Underwriting Work For Mortgages

Debtors seeking to reduce their short-term rate and/or payments; house owners who prepare to move in 3-10 years; high-value borrowers who do not desire to bind their money in home http://elliotvwbt003.yousher.com/an-unbiased-view-of-how-do-mortgages-work-in-the-us equity. Debtors who are unpleasant with unpredictability; those who would be economically pressed by higher home loan payments; borrowers with little house equity as a cushion westlake financial el paso tx for refinancing.

Long-term home loans, financially inexperienced customers. Buyers acquiring high-end homes; borrowers setting up less than 20 percent down who want to prevent paying for home mortgage insurance coverage. Homebuyers able to make 20 percent deposit; those who expect increasing home values will allow them to cancel PMI in a few years. Debtors who require to obtain a swelling amount money for a specific function.

Those paying an above-market rate on their primary home mortgage may be much better served by a cash-out re-finance. Borrowers who need need to make regular expenditures over time and/or are unsure of the total quantity they'll require to borrow. Debtors who require to obtain check here a single swelling amount; those who are not disciplined in their costs routines (why is there a tax on mortgages in florida?). how do reverse mortgages work in utah.

The Best Strategy To Use For How Do Home Equity Mortgages Work

But when you die, sell your home or move out, you, your partner or your estate, i. e., your children, should pay back the loan. Doing that might indicate selling the house to have adequate cash to pay the accrued interest (buy to let mortgages how do they work). If you're lured to get a reverse home mortgage, be sure to do your homework thoroughly.

// Reverse Home Loan Disadvantages and Benefits: Your Guide to Reverse Mortgage Pros and ConsFor many individuals, a Reverse Home Mortgage is an excellent method to increase their financial wellness in retirement favorably affecting lifestyle. And while there are numerous advantages to the product, there are some downsides reverse mortgage disadvantages.

Nevertheless, there are some disadvantages The in advance fees (closing and insurance costs and origination fees) for a Reverse Mortgage are considered by many to be rather high partially greater than the expenses charged for refinancing for example. Furthermore, FHA program modifications in Oct-2017 increased closing costs for some, but ongoing maintenance expenses to hold the loan reduced for all.

For more info on the costs charged on Reverse Home mortgages, seek advice from the Reverse Home mortgage rates and charges short article. Also, if costs concern you, attempt speaking to numerous Reverse Home mortgage lending institutions you might discover a much better deal from one over another. There are no month-to-month payments on a Reverse Home mortgage. As such, the loan amount the quantity you will eventually have to pay back grows bigger gradually.

Nevertheless, the quantity you owe on the loan will never exceed the worth of the house when the loan becomes due. Many Reverse Mortgage borrowers value that you don't have to make monthly payments which all interest and costs are funded into the loan. These features can be viewed as Reverse Home mortgage disadvantages, but they are likewise huge benefits for those who wish to remain in their home and enhance their immediate finances.

The HECM loan limit is presently set at $765,600, implying the amount you can borrow is based upon this worth even if your house is valued for more. Your actual loan quantity is identified by an estimation that utilizes the assessed worth of your home (or the loaning limit above, whichever is less), the quantity of money you owe on the house, your age, and present interest rates.

The 3-Minute Rule for How Do Right To Buy Mortgages Work

With a standard mortgage you borrow cash in advance and pay the loan down gradually. A Reverse Mortgage is the opposite you build up the loan with time and pay everything back when you and your spouse (if appropriate) are no longer residing in the home. Any equity staying at that time belongs to you or your successors.

Many experts shunned the product early on believing that it was a bad offer for elders but as they have actually learnt more about the information of Reverse Mortgages, experts are now welcoming it as a valuable monetary planning tool. The main advantage of Reverse Home mortgages is that you can remove your standard home mortgage payments and/or access your home equity while still owning and residing in your house.

Secret advantages and advantages of Reverse Home mortgages include: The Reverse Mortgage is a greatly flexible item that can be utilized in a variety of ways for a variety of different types of borrowers. Families who have a monetary need can customize the product to de-stress their finances. Homes with sufficient resources might think about the product as a financial planning tool.

Unlike a home equity loan, with a Reverse Home Home loan your home can not be taken from you for factors of non-payment there are no payments on the loan until you permanently leave the house. Nevertheless, you must continue to pay for maintenance and taxes and insurance coverage on your house.

With a Reverse Home mortgage you will never ever owe more than your home's worth at the time the loan is repaid, even if the Reverse Home mortgage lenders have actually paid you more money than the value of the house (how do owner financing mortgages work). This is an especially useful benefit if you protect a Reverse Home mortgage and then home costs decrease.

How you use the funds from a Reverse Mortgage depends on you go traveling, get a listening devices, purchase long term care insurance coverage, spend for your children's college education, or just leave it sitting for a rainy day anything goes. Depending on the kind of loan you pick, you can receive the Reverse Home loan money in the kind of a lump sum, annuity, line of credit or some combination of the above.

The Best Strategy To Use For How Do Construction Mortgages Work

With a Reverse Home loan, you retain house ownership and the capability to live in your house. As such you are still required to keep up insurance coverage, property taxes and upkeep for your home. You can live in your house for as long as you want when you secure a Reverse Home loan.

It is handled by the Department of Real Estate and Urban Affairs and is federally guaranteed. This is very important given that even if your Reverse Home mortgage lender defaults, you'll still get your payments. Depending on your circumstances, there are a range of manner ins which a https://fortune.com/best-small-workplaces-for-women/2020/wesley-financial-group/ Reverse Home mortgage can assist you preserve your wealth.

This locks in your existing home value, and your reverse mortgage credit line in time may be bigger than future property values if the market decreases. Personal finance can be made complex. You wish to maximize returns and lessen losses. A Reverse Home mortgage can be among the my timeshare expert reviews levers you use to maximize your overall wealth.

( KEEP IN MIND: Social Security and Medicare are not affected by a Reverse Mortgage.) Because a Reverse House Home mortgage loan is due if your house is no longer your primary house and the in advance closing costs are typically higher than other loans, it is not a good tool for those that prepare to move quickly to another house (within 5 years).

And it is true, a Reverse Mortgage reduces your home equity affecting your estate. Nevertheless, you can still leave your home to your successors and they will have the alternative of keeping the home and refinancing or paying off the mortgage or selling the home if the home deserves more than the amount owed on it - how do mortgages work in monopoly.

Studies show that more than 90 percent of all households who have actually protected a Reverse Home mortgage are incredibly delighted that they got the loan. People state that they have less tension and feel freer to live the life they desire. Discover more about the costs connected with a Reverse Home mortgage or instantly estimate your Reverse Home loan amount with the Reverse Home Mortgage Calculator.

What Does How Do Commercial Mortgages Work Do?

A reverse home mortgage is a loan product that permits senior house owners to convert house equity into cash. Many reverse home mortgages are offered by the Federal Housing Administration (FHA), as part of its Home Equity Conversion Home Loan (HECM) program. With a reverse home mortgage, you get money from your home mortgage business as a loan secured versus the equity in your home.

The Main Principles Of What Is The Maximum Debt-to-income Ratio Permitted For Conventional Qualified Mortgages

The main benefit of this program (and it's a huge one) is that customers can receive 100% financing for the purchase of a house. That implies no deposit whatsoever. The United States Department of Farming (USDA) uses a loan program for rural customers who satisfy specific earnings requirements. The program is managed by the Rural Housing Service (RHS), which becomes part of the Department of Farming.

The AMI differs by county. See the link listed below for details. Integrating: It's important to keep in mind that debtors can integrate the types of home mortgage types discussed above. For instance, you may choose an FHA loan with a set interest rate, or a traditional home mortgage with nashville xm radio an adjustable rate (ARM).

Depending on the amount you are attempting to obtain, you might fall under either the jumbo or conforming category. Here's the difference in between these 2 home mortgage types. A conforming loan is one that fulfills the underwriting standards of Fannie Mae or Freddie Mac, especially where size is concerned. Fannie and Freddie are the two government-controlled corporations that purchase and offer mortgage-backed securities (MBS). Property owners seeking a house equity loan who would likewise benefit from re-financing their current mortgage. Property owners seeking a house equity loan who would get little or no cost savings from re-financing their existing home mortgage. Underwater debtors or those with less than 20 percent house equity; those seeking to refinance at a lower rates of interest; customers with an ARM or upcoming balloon payment who wish to convert to a fixed-rate loan.

Newbie homebuyers, buyers who can not install a big deposit, borrowers purchasing a low- to mid-priced home, buyers seeking to purchase and enhance a house with a single home mortgage (203k program). Debtors acquiring a high-end house; those able to put up a deposit of 10 percent or more.

Non-veterans; veterans and active service members who have actually exhausted their basic privilege or who are aiming to buy financial investment home. Novice buyers with young families; those currently living in congested or out-of-date housing; citizens of backwoods or little communities; those with restricted incomes Urban dwellers, families with above-median incomes; bachelors or couples without children.

One of the first concerns you are bound to ask yourself when you wish to buy a home is, "which home mortgage is right for me?" Essentially, purchase and re-finance loans are divided into fixed-rate or variable-rate mortgages - which mortgages have the hifhest right to payment'. When you pick fixed or adjustable, you will also require to think about the loan term.

How Would A Fall In Real Estate Prices Affect The Value Of Previously Issued Mortgages? Things To Know Before You Buy

Long-lasting fixed-rate mortgages are the staple of the American mortgage market. With a fixed rate and a repaired monthly payment, these loans offer the most stable and predictable expense of homeownership. This makes fixed-rate mortgages incredibly popular for property buyers (and refinancers), especially sometimes when interest rates are low. The most common term for a fixed-rate home mortgage is thirty years, however shorter-terms of 20, 15 and even ten years are likewise offered.

Since a higher monthly payment http://edgarjlss664.lowescouponn.com/some-ideas-on-who-is-specialty-services-for-home-mortgages-you-need-to-know restricts the quantity of home mortgage an offered income can support, many property buyers decide to spread their regular monthly payments out over a 30-year term. Some home loan lending institutions will enable you to personalize your home mortgage term to be whatever length you want it to be by changing the regular monthly payments.

Considering that regular monthly payments can both rise and fall, ARMs carry threats that fixed-rate loans do not. ARMs are helpful for some borrowers-- even first time debtors-- but do need some additional understanding and diligence on the part of the consumer (what are the interest rates on 30 year mortgages today). There are knowable threats, and some can be handled with a little planning.

Standard ARMs trade long-lasting stability for routine modifications in your interest rate and month-to-month payment. This can work to Click for source your advantage or disadvantage. Standard ARMs have rate of interest that change every year, every 3 years or every 5 years. You might hear these described as "1/1," "3/3" or " 5/5" ARMs.

For instance, initial rates of interest in a 5/5 ARM is repaired for the very first five years (when does bay county property appraiser mortgages). After that, the rates of interest resets to a new rate every 5 years up until the loan reaches the end of its 30-year term. Standard ARMs are generally provided at a lower initial rate than fixed-rate mortgages, and typically have payment terms of thirty years.

Naturally, the reverse holds true, and you could wind up with a greater rate, making your mortgage less budget friendly in the future. Note: Not all lenders offer these items. Standard ARMs are more favorable to homebuyers when rate of interest are fairly high, given that they offer the possibility at lower rates in the future.

Not known Details About What Bank Keeps Its Own Mortgages

Like standard ARMs, these are normally offered at lower rates than fixed-rate home loans and have total repayment terms of 30 years. Since they have a range of fixed-rate periods, Hybrid ARMs provide debtors a lower initial interest rate and a fixed-rate home mortgage that fits their anticipated timespan. That said, these items carry risks given that a low set rate (for a few years) might pertain to an end in the middle of a higher-rate climate, and regular monthly payments can jump.

Although frequently discussed as though it is one, FHA isn't a home loan. It stands for the Federal Housing Administration, a government entity which basically runs an insurance swimming pool supported by charges that FHA home loan customers pay. This insurance coverage swimming pool essentially removes the risk of loss to a lending institution, so FHA-backed loans can be provided to riskier borrowers, especially those with lower credit scores and smaller deposits.

Popular amongst novice property buyers, the 30-year fixed-rate FHA-backed loan is offered at rates even lower than more standard "adhering" mortgages, even in cases where borrowers have weak credit. While down payment requirements of as little as 3.5 percent make them especially attractive, customers must pay an in advance and annual premium to fund the insurance coverage pool noted above.

For more information about FHA mortgages, check out "Advantages of FHA home loans." VA home mortgage are mortgages guaranteed by the U.S. Department of Veterans Affairs (VA). These loans, issues by personal lending institutions, are provided to eligible servicemembers and their households at lower rates and at more beneficial terms. To figure out if you are qualified and to learn more about these home loans, visit our VA mortgage page.

Fannie Mae and Freddie Mac have limitations on the size of home mortgages they can buy from loan providers; in the majority of areas this cap is $510,400 (as much as $765,600 in particular "high-cost" markets). Jumbo home mortgages been available in fixed and adjustable (standard and hybrid) varieties. Under policies imposed by Dodd-Frank legislation, a meaning for a so-called Qualified Home mortgage was set.

![]()

QMs also permit for borrower debt-to-income level of 43% or less, and can be backed by Fannie Mae and Freddie Mac. Presently, Fannie Mae and Freddie Mac are utilizing special "momentary" exemptions from QM rules to purchase or back home loans with DTI ratios as high as 50% in some situations.

Some Ideas on What Are The Interest Rates On Reverse Mortgages You Should Know

The location is fourth in the United States in brand-new facilities including GE Aviation's new 420,000 square-foot Class An office school and a brand-new 80,000 sq feet Proton Treatment Center for cancer research. Cincinnati has also finished a $160 Million dollar school expansion. In 2019, the typical regular monthly rent for 3 bedroom houses in Cincinnati was $1,232, which is 0.75% of the purchase price of $165,000.

The Cincinnati metro area has the fourth biggest number of brand-new facilities in the U.S. including GE Air travel's new 420,000 square-foot Class An office school and a brand-new 80,000 sq feet Proton Therapy Center for cancer research. Job growth in Cincinnati is growing 40% faster than the nationwide average. The Cincinnati metro population has grown 3.58% over the past 8 years.

And with an expense of living that is below the nationwide average, this trend will likely continue. In Cincinnati, it's still possible to acquire fully refurbished capital homes in good communities for $123,000 to Click for source $150,000. At RealWealth we connect financiers with residential or commercial property teams in the Cincinnati metro location. Presently the groups we deal with deal the following rental investments: (1) (2) If you want to see Sample Residential or commercial property Pro Formas, link with one of the groups we deal with in Cincinnati, or speak with among our Investment Counselors about this or other markets, end up being a member of RealWealth free of charge.

Known for its imposing skyscrapers and Fortune 500 companies, the Windy City is one of the couple of remaining U.S. markets where you can still discover excellent financial investment chances. With greater realty costs and lower-than-average task and population development, Chicago may not look like a "good" location to invest in property.

When concentrating on finding the highest capital development and capital, you'll find some areas provide houses at $128,000 to $210,000 with leas as high as 1.13% (above nationwide average) of the purchase rate monthly.! All of this is great news for financiers lookin for under market worth residential or commercial properties, with incredible monthly capital, and poised for consistent appreciation.

The 10-Second Trick For What Is A Bridge Loan As Far As Mortgages Are Concerned

The average price of the average 3 bedroom home in the Chicago metro location was $210,000 - how do mortgages work with married https://postheaven.net/sulannt0gx/lots-of-or-all-of-the-products-featured-here-are-from-our-partners-who couples varying credit score. This is 5% less than the national average of $222,000 for 3 bedroom houses. wesley browning In the areas where RealWealth members invest, the mean purchase rate was just $128,000 in 2019, which is 42% more affordable than the nationwide average.

83% of Chicagoans reside in a house for 1 year or more. Chicago is house to 30 Fortune 500 business and boasts a $500 billion GDP, which is more than that of Norway and Belgium combined! Chicago is the 3rd biggest city in the United States and among the leading 5 most economically powerful cities worldwide.

In the previous year, Chicago added 37,900 new jobs to their economy. Property prices have actually skyrocketed within Chicago's city limitations, triggering people to vacate the city and into the suburbs. As a result, prices in a few of these neighborhoods continue to increase. While Chicago's population development is well below the nationwide average, it is very important to keep in mind that it's still consistently growing, which his an excellent indication for those wanting to purchase more steady markets.

The mean sale price for a home in Chicago is $210,000, however it's still possible to find houses for sale in mid-level communities in between $128,000 and $210,000. In the neighborhoods where RealWealth members invest, 3 bedroom homes rent for $1,450 each month, which is 1.13% of the $128,000 typical purchase cost.

This suggests there are fantastic chances for capital in Chicago, and a strong possibility of appreciation too. At RealWealth we link investors with residential or commercial property teams in the Chicago metro location. Currently the groups we deal with deal the following rental investments: (1) (2) consisting of some. If you 'd like to see Sample Property Pro Formas, connect with one of the teams we deal with in Chicago, or talk to one of our Investment Therapists about this or other markets, end up being a member of RealWealth totally free.

The Best Strategy To Use For How Is Freddie Mac Being Hels Responsible For Underwater Mortgages

Unsure if section 8 is the right choice for you? Take a look at our detailed guide: Is Section 8 Great For Landlords or Not? With a metro area of over 2.1 million individuals, Indianapolis is the 2nd biggest city in the Midwest and 14th largest in the U.S. The city has poured billions of dollars into revitalization and now ranks among the finest downtowns and most habitable cities, according to Forbes.

Indy also has a strong, varied job market, terrific schools and universities, and a lot of sports tourist attractions. In 2019, the mean regular monthly rent for three bed room homes in Indianapolis was $1,172, which is 0.71% of the purchase rate of $164,400. This is a little lower than the nationwide price-to-rent ratio of 0.75%.

Reward: you can purchase like-new residential or commercial properties for just $80,000 $350,000. Metro Population: 2.1 MMedian Household Income: $68,000 Existing Median Home Rate: $164,400 Mean Lease Per Month: $1,1721-Year Task Development Rate: 0.81% 7-Year Equity Growth Rate: 45.00% 8-Year Population Growth: 8.25% Joblessness Rate: 3.1% 3 Fortune 500 Business have their head office in Indianapolis. 7 modern "Qualified Innovation Parks" with tax rewards to start-ups.

Indy is the ONLY U.S. city to have actually specialized employment concentrations in all 5 bioscience sectors evaluated in the study: farming feedstock and chemicals; bioscience-related distribution; drugs and pharmaceuticals; medical gadgets and devices; and research, screening, and medical laboratories - how many mortgages in a mortgage backed security. Like many of the markets on this list, Indianapolis has job growth, population development and cost.

Here's a wrap-up: Indianapolis is among the fastest growing hubs for innovation, bioscience and Fortune 500 business in the country. In reality, Indy is the ONLY U.S. city to have actually specialized employment concentrations in all five bioscience sectors assessed in the study: farming feedstock and chemicals; bioscience-related distribution; drugs and pharmaceuticals; medical gadgets and devices; and research, screening, and medical labs.

How Many Mortgages In One Fannie Mae Fundamentals Explained